Changes to the Disability Support Pension have gutted Australia's social safety net

Most people are saving too much for retirement. But why? One of the reasons is because the superannuation system in forces Australians to self-insure against bad outcomes like needing to retire early.

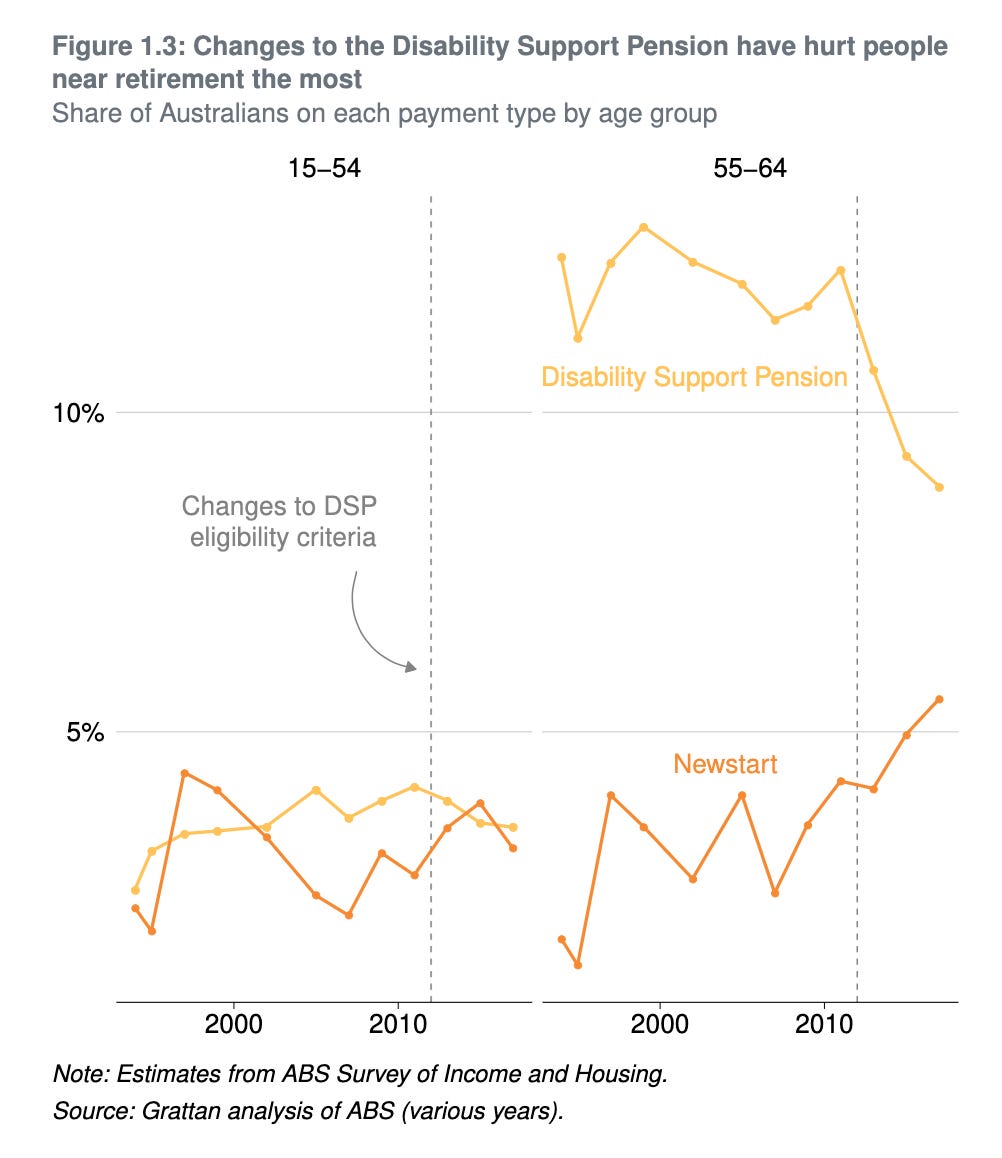

People who are forced to retire early, such as carers or those with a disability, used to be able to rely on the Carer Payment or the Disability Support Pension. But as shown in in the graph below, recent changes to eligibility requirements for the Disability Support Pension mean fewer older Australians access the scheme then previously. And Newstart remains inadequate, having not been increased for the past two decade

Forcing all Australians to self-insure by saving even more for retirement, just in case they retire early, makes them poorer while working and is simply a recipe for larger inheritances.

Eligibility requirements for the Disability Support Pension were tightened in 2012, to the detriment of many near-retirees with musculoskeletal health problems. In 2009, about 12 per cent of 55-64 year-olds were on the Disability Support Pension. By 2017 that number had fallen to 9 per cent. The decline coincides with an increase in the number of older people on Newstart.

Newstart has also become woefully inadequate as a safety net for unemployed Australians. Unlike wages or pensions, Newstart has not increased in real terms in more than 20 years. While the Age Pension is indexed to wages, Newstart only increases with inflation. This has ‘squeezed’ the living standards of people living on Newstart relative to the rest of the population.59 A typical single person on Newstart receives just $39 a day, about 18 per cent of average (male) earnings.

Households of working age receiving welfare payments – primarily Newstart – are under much more financial stress than households receiving other welfare payments.

This is an adapatation/exert based on research in