Most of Australia's retirees are financially secure

Every once in a while a commentator in Australia will log-in to the OECD website and pull a statistics which shows that Australian retirees are doing it tough compared to our gloabl peers. But because of how our retirement income system works these statitistics are misleading. If you own your own home (and most retirees do), you’re retirement in Australia is secure.

In 2013, the OECD poverty measure found that 26 per cent of Australians aged 65 and older suffered income poverty in 2013, compared to 13 per cent across all OECD countries.

But there are a number of problems with the OECD measure. It does not take into account drawdowns on savings outside super, and does not adequately account for housing costs. And like other poverty benchmarks, small changes in income can produce radically different rates of poverty.

Old-age poverty in Australia under the OECD’s relative measure is extremely volatile from year to year, because the Australian Age Pension sits right on the edge of the OECD’s poverty benchmark. For example, old-age poverty in Australia apparently fell sharply from 22 per cent in 2011 to 12 per cent in 2018.113 But the big apparent shift merely reflected the maximum rate of the Age Pension (including related supplements) oscillating around the benchmark of 50 per cent of median incomes. The minimum pension in many other countries is much lower and in some is available only to people who have been employed for most of the time while they were of working age. As a result, Australia has far fewer retirees in severe poverty whose income is much less than the OECD’s benchmarks.

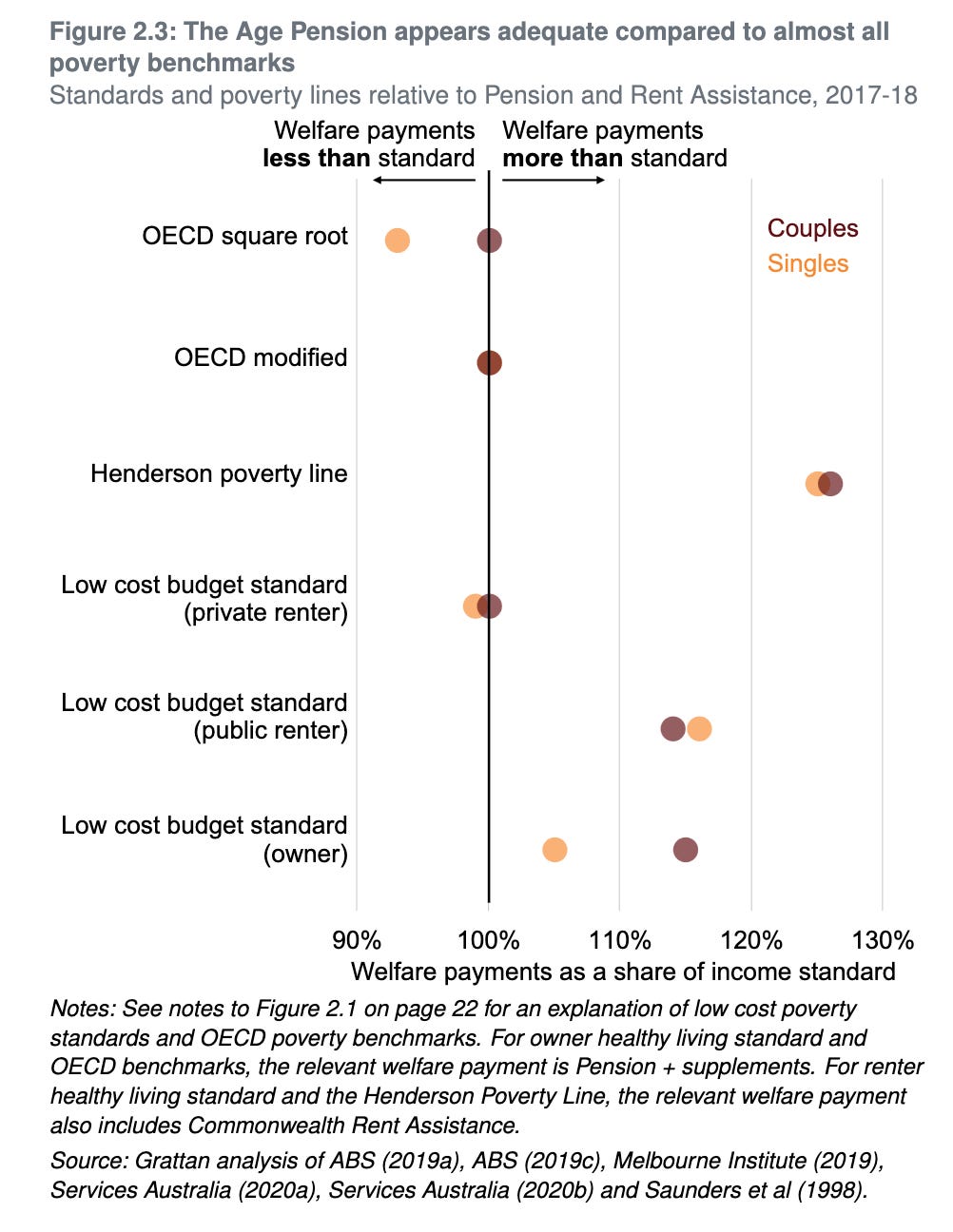

This clustering close to the benchmark also means that outcomes on the measure depend a lot on somewhat arbitrary definitions. For example, the apparent poverty rate in 2017-18 changes from 14 per cent to 25 per cent, depending on how households with different family sizes are compared. Even then, the income poverty measure can be misleading. The 14 per cent of senior Australians classified as living in poverty on the ABS preferred definition are often people of significant means who are ineligible to receive a maximum-rate Age Pension and whose drawdowns of existing savings are not counted as income. More than half of over-65s classified as living in poverty in 2017-18 based on the ABS preferred definition were among the wealthiest half of all retirees.

In many other OECD countries the depth of poverty for older-aged people is much greater - meaning that instead of straddling the poverty line, low-income people sink far below it.

A more reliable measure of poverty for retirees, especially renters, is income poverty after housing. This is the proportion of households that have less than half the median disposable income once housing is taken into account. To account for housing, this measure uses a standard ABS estimate of the value home-owners get from not having to pay rent. The measure raises the income of home-owners significantly, while exposing the tough economic circumstances faced by many renters. On this measure, about 10 per cent of Australians aged 65 and older live in poverty after taking account of their housing costs, but results vary wildly by housing tenure. About 60 per cent of retired Australians who rent and live alone are in poverty after housing costs. In contrast to less than 10 per cent of retired homeowners without a mortgage.

Retirees in Australia also feel financially comfortable. Most retirees have paid off their mortgage, and no longer have the financial stress of bringing up children. They are far less likely to suffer financial stress such as not being able to pay a bill on time, and are more likely than working-age households to say they feel financially comfortable Just as retirees are less stressed about essentials, their discretionary expenditure is also less financially constrained than that of working-age people. Retirees are less likely to miss out, due to cost, on things like taking a holiday. Retirement is a particular relief for low-income earners, whose income typically increases in retirement with access to the Age Pension.

Rather than running out of money each week and dipping excessively into savings, higher-income Australians maintain their nest egg well into retirement. Most retirees never spend a large part of the savings that they have on the day they retire. Many retirees seem reluctant to draw down on their capital, and instead live on the income their savings generate. While precautionary savings may explain part of retirees’ savings behaviour (Section 1.6 on page 17), the combination of a lack of spending and high rates of financial satisfaction suggests that retirees’ needs are being met.

Home-owning retirees receive a significant financial windfall because most of the value of their home is effectively excluded from the Age Pension assets testBut . For pensioners who don’t own their own home, Rent Assistance is a fortnightly payment that can help bridge the gap.

But rent assistance is not high enough. The maximum Rent Assistance payment is indexed in line with CPI, but rents have been growing faster than CPI over the long term. Between June 2003 and June 2019, CPI increased by about 46 per cent, while average (quality adjusted) rents increased by about 65 per cent.

The Age Pension is sufficient for most retirees to have an income above most measures of poverty. But it is not sufficient for renter households. Commonwealth Rent Assistance should be increased by about 40 per cent, to overcome its decline relative to average rents over the past two decades. This would be the most targeted way to alleviate poverty among retirees.

This is an adapted exerpt from Coates, B. and Nolan, J. (2020). Balancing act: managing the trade-offs in retirement incomes policy. Grattan Institute.